GLP-1 Receptor Agonist Market Forecast 2026–2036: Market Expansion Driven by Cardiometabolic Demands

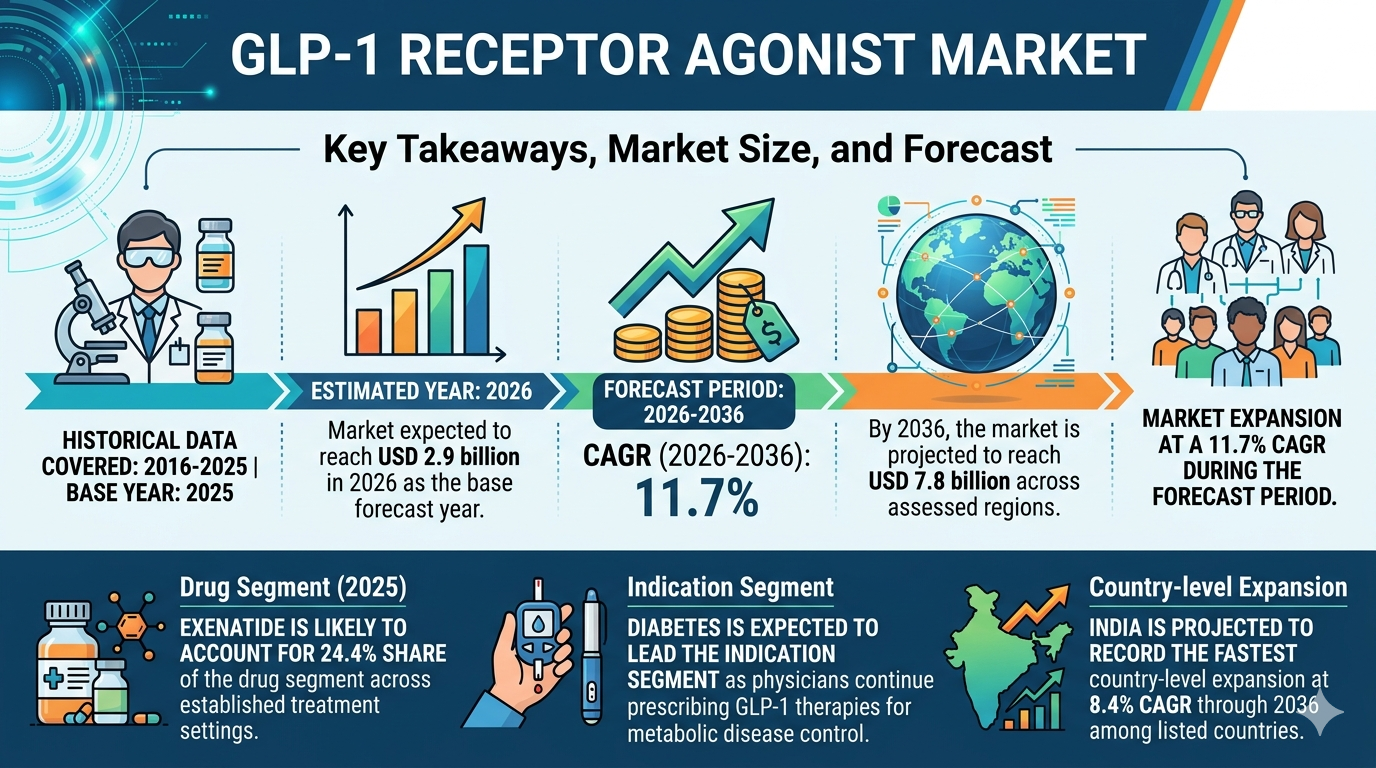

The global GLP-1 receptor agonist market is projected to witness strong expansion over the next decade, supported by widening clinical indications and rapid pharmaceutical innovation. The market is expected to grow steadily, reaching approximately USD 7.8 billion by 2036, registering a CAGR of 11.7%, according to the latest analysis by Future Market Insights (FMI).

Market growth is being shaped by increasing prevalence of type 2 diabetes and obesity, growing clinical recognition of cardiorenal-metabolic benefits, and the rapid adoption of advanced drug formulations. GLP-1 receptor agonists have evolved from optional second-line diabetes treatments into essential cornerstone therapies across metabolic and cardiovascular disease management. While traditional parenteral (injectable) delivery methods continue to dominate patient usage, manufacturers are increasingly launching oral alternatives to comply with modern patient expectations and improve long-term treatment compliance.

GLP-1 Receptor Agonist Market Snapshot (2026–2036)

Market size outlook toward 2036: USD 7.8 billion

Forecast CAGR: 11.7%

Dominant drug segment: Exenatide (~24.4% market share)

Fastest-growing segment: Next-generation oral formulations

Key growth countries: United States, United Kingdom, China, India

Primary demand channel: Hospital pharmacies (~34.0% market share)

Momentum in the Market

Beginning from steady baseline adoption levels, the GLP-1 receptor agonist market demonstrates accelerated growth throughout the forecast period as therapeutic approvals expand beyond glycemic control. Between 2026 and 2036, expanding clinical pipelines and a rising global patient pool seeking long-term metabolic management are expected to significantly boost demand for integrated therapeutic interventions. Increasing urbanization and higher rates of lifestyle-induced metabolic disorders are encouraging healthcare systems and payers to prioritize early disease-modifying technologies.

From 2036 onward, innovation in non-invasive delivery pathways and the integration of these agents into multi-receptor hormone therapies (such as dual GIP/GLP-1 or triple receptor agonists) is expected to further strengthen market expansion. Highly effective small-molecule weight loss treatments capable of adapting metabolic response without strict fasting windows are emerging as key differentiators in new pharmaceutical portfolios.

The Reasons Behind the Market’s Growth

Demand for GLP-1 receptor agonists is rising due to multiple structural and clinical factors reshaping the global healthcare ecosystem.

Evolving Regulatory Frameworks and Approvals

Regulatory bodies are enforcing updated clinical guidelines that fast-track GLP-1 indications for adolescent obesity and cardiovascular risk mitigation, integrating them deeply into therapeutic standards.

Widening Cardiometabolic Indications

Clinical evidence demonstrating reduced major adverse cardiovascular events (MACE) and slowed kidney disease progression is driving large-scale provider adoption of these therapies.

Rising Patient and Prescriber Awareness

End-users and physicians are prioritizing drugs equipped with dual metabolic benefits, accelerating adoption across both diabetes and weight-reduction patient demographics.

Oral Formulation Expansion

The rise of daily oral pills is creating demand from needle-averse patients, bypassing the cold-chain shipping and storage complexities required by traditional subcutaneous injectables.

Top Segment Application Type

Diabetes Management Leads Market Demand

Type 2 diabetes accounts for the majority of prescription volume across international markets, supported by high baseline disease prevalence and regulatory mandates reinforcing its cardiorenal protection.

Drug and Therapy Analysis

Exenatide: ~24.4% market share driven by established clinical presence.

Semaglutide: Massive commercial growth supported by multi-indication blockbusters (Ozempic/Wegovy).

Liraglutide: Major pediatric and adolescent clinical adoption segment.

Oral GLP-1s: Fastest-growing segment following recent regulatory approvals.

Regional Development: Manufacturing and Healthcare Ecosystems Drive Expansion

Global regions are rapidly evolving into scaled hubs for metabolic therapies, supported by expanding public reimbursement policies and generic manufacturing capabilities.

United States & United Kingdom: Commercial and regulatory leaders driving digital monitoring integrations.

China & India: Rapidly expanding patient access and generic/biosimilar development infrastructure.

Localized manufacturing partnerships between global bio-pharma companies and regional suppliers are improving cost efficiency while accelerating delivery system innovation.

Challenges, Trends, Opportunities, and Drivers

Drivers

- Mandated cardiorenal clinical guidelines

- Rising global diabetes and obesity prevalence

- Increasing preventative health awareness

- Expansion of oral peptide delivery platforms

Opportunities

- Dual and triple-receptor co-agonists

- Pediatric obesity intervention pathways

- Multi-benefit metabolic disease management

- Integration with digital patient support apps

Trends

- Transition toward once-weekly or extended-interval dosing

- Oral alternatives with minimal food restrictions

- Surging direct-to-consumer digital prescription models

- Increased availability of bio-similars upon patent expiration

Challenges

- Cost pressures for uninsured patient segments

- Gastrointestinal side effects during early therapy initiation

- Supply chain manufacturing bottlenecks for auto-injector pens

Country Growth Outlook

The market’s growth trajectory is closely tied to therapeutic commercialization and healthcare coverage implementation across key economies:

- United States: Market leadership via high therapeutic adoption and insurance integration.

- United Kingdom: Expanding public health system clinical recommendation pathways.

- China: Government-led healthcare initiatives scaling metabolic drug accessibility.

- India: Surging private market demand and exceptional clinical awareness growth.

The Competitive Environment

The global GLP-1 receptor agonist market is moderately consolidated, with tier-one pharmaceutical providers competing through molecule innovation, outcome trials, and pricing strategies. Leading companies include:

- Novo Nordisk A/S

- Eli Lilly and Company

- AstraZeneca

- Sanofi

These players are investing heavily in multi-receptor assets, stable oral platforms, and high-volume manufacturing lines while forming partnerships with telemedicine ecosystems to strengthen supply chains and accelerate therapy compliance.

Future Outlook: Toward Integrated and Non-Invasive Metabolic Care

The GLP-1 receptor agonist market is entering a transformative decade shaped by molecule optimization, non-injectable options, and preventative cardiometabolic strategies. Future therapies are expected to function as integrated metabolic modules working alongside digital health platforms to prevent long-term organ damage. As medical systems mature and chronic care access strengthens, GLP-1 therapies will remain central to achieving healthier and more sustainable healthcare outcomes globally.

Explore the full report on the official Future Market Insights website: https://www.futuremarketinsights.com/reports/glp-1-receptor-agonist-market