Oil and Gas Sensor Market to Surpass USD 14.9 Billion by 2035

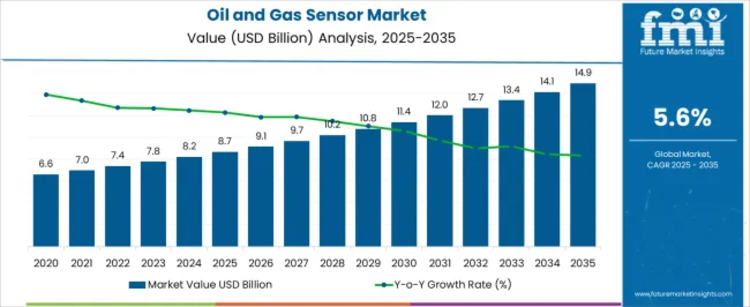

The global oil and gas sensor market is entering a new phase of industrial modernization as energy companies intensify investments in digital infrastructure, real-time monitoring, predictive maintenance, and operational resilience. According to the latest analysis by Future Market Insights, the market is projected to expand from USD 8.7 billion in 2025 to USD 14.9 billion by 2035, registering a CAGR of 5.6% during the forecast period.

The evolution of oil and gas operations toward automated, connected, and data-driven environments is significantly increasing the deployment of high-performance sensing technologies. Sensors are becoming critical components across exploration, production, transportation, refining, and environmental monitoring applications, helping operators improve uptime, enhance safety standards, reduce emissions, and optimize energy efficiency.

Get detailed market forecasts, competitive benchmarking, and pricing trends: https://www.futuremarketinsights.com/reports/sample/rep-gb-19156

Featured Snippet: Key Market Insights

- Market Size (2025): USD 8.7 Billion

- Forecast Value (2035): USD 14.9 Billion

- CAGR (2025–2035): 5.6%

- Leading Type Segment: Pressure Sensors (37.8% share)

- Leading Connectivity: Wired Sensors (61.4% share)

- Leading Sector: Upstream Operations (52.6% share)

- Top Growth Regions: North America, Asia-Pacific, Europe

- Primary Growth Drivers: Industrial automation, remote monitoring, predictive maintenance, environmental compliance, IoT integration

Market Overview: Intelligent Sensing Redefines Energy Operations

The oil and gas sensor market continues to evolve as energy producers increasingly rely on intelligent instrumentation to improve operational visibility and process control.

Sensors are enabling real-time measurement of pressure, temperature, vibration, gas concentration, fluid levels, and equipment conditions across critical infrastructure. Their integration into digital oilfields and automated industrial ecosystems is reducing operational risk while strengthening decision-making capabilities.

Growing emphasis on sustainability and environmental accountability is also accelerating demand for advanced sensing platforms capable of monitoring emissions and supporting regulatory compliance.

Key Market Drivers

- Expansion of Automation and Digital Oilfields

Energy operators are adopting advanced monitoring systems to improve productivity and asset utilization.

Emerging technologies include:

- IoT-enabled sensor networks

- AI-driven predictive maintenance

- Cloud-based industrial analytics

- Edge-enabled monitoring architectures

These capabilities support faster response times, lower downtime, and enhanced production continuity.

- Regulatory Focus on Safety and Emission Monitoring

Global regulatory frameworks are placing increased pressure on operators to improve environmental performance and worker safety.

Sensor systems help organizations:

- Detect hazardous gas leaks

- Monitor methane emissions

- Maintain process integrity

- Ensure compliance with operational standards

- Rising Investment in Remote Monitoring Infrastructure

Remote operations are becoming increasingly important across upstream and offshore environments.

Connected sensing platforms allow operators to:

- Monitor equipment remotely

- Reduce manual inspections

- Improve maintenance scheduling

- Enable real-time operational intelligence

Segment Analysis

Pressure Sensors Lead Market Adoption

Pressure sensors remain the dominant category with 37.8% market share due to their critical role across drilling, extraction, transportation, and refining operations.

Key advantages include:

- Continuous pressure tracking

- Improved equipment protection

- Enhanced process reliability

- Better operational efficiency

Demand for ruggedized and digitally calibrated pressure sensors continues to rise.

Wired Connectivity Maintains Leadership

The wired segment accounts for 61.4% of deployment, supported by superior signal stability and secure communication performance.

Benefits include:

- Reliable data transmission

- Lower communication interference

- Strong compatibility with industrial control systems

- Enhanced cybersecurity performance

Although wireless adoption is increasing, wired infrastructure remains preferred for mission-critical environments.

Upstream Operations Drive Demand

Upstream applications contribute 52.6% of total market value, supported by increased drilling activity and expanding exploration investments.

Sensors play a major role in:

- Reservoir monitoring

- Production optimization

- Pressure management

- Equipment condition monitoring

Regional Outlook

North America

North America continues to lead technological adoption due to:

- Mature oilfield infrastructure

- Strong investment in digital transformation

- Tight environmental compliance requirements

The United States remains a major contributor with increasing deployment of intelligent gas detection and predictive monitoring technologies.

Europe

Europe’s market growth is supported by:

- Industrial sustainability initiatives

- Carbon reduction programs

- Advanced automation deployment

- Strong environmental monitoring regulations

Asia-Pacific

Asia-Pacific is emerging as one of the fastest-growing regions owing to:

- Expanding industrialization

- Infrastructure modernization

- Growth in exploration activity

- Increased energy security investments

China, Japan, India, and South Korea continue expanding adoption of advanced industrial sensing technologies.

Technology Trends Transforming the Industry

Several innovations are reshaping sensor deployment across oil and gas infrastructure:

- IoT-integrated remote monitoring systems

- Multi-parameter sensing platforms

- AI-enabled predictive diagnostics

- Digital twins for infrastructure simulation

- Miniaturized industrial sensors

- Emission tracking and methane detection technologies

These developments are enabling a more connected, intelligent, and resilient industrial ecosystem.

Challenges Across the Market

High Implementation Costs

Deployment of advanced sensing environments requires:

- Infrastructure modernization

- Integration with legacy systems

- Skilled technical expertise

- Long deployment cycles

Complexity of Industrial Integration

Operators continue facing challenges associated with:

- Calibration requirements

- Data interoperability

- Cybersecurity concerns

- System maintenance demands

Opportunities: Building the Connected Energy Future

Future growth opportunities include:

- Smart oilfield deployments

- Autonomous monitoring systems

- Energy-efficient sensing platforms

- Cloud-based operational analytics

- Emission reduction technologies

- Predictive maintenance ecosystems

Organizations investing in scalable and intelligent sensing infrastructure are expected to strengthen competitive positioning.

Competitive Landscape

The oil and gas sensor market remains highly competitive, with industry leaders emphasizing product innovation, automation capabilities, and strategic expansion.

Leading Companies

- Honeywell International Inc.

- Siemens AG

- Emerson Electric Co.

- ABB Ltd.

- Yokogawa Electric Corporation

- Bosch Sensortec GmbH

- Drägerwerk AG & Co. KGaA

- General Electric Company

- Teledyne Technologies Incorporated

- Endress+Hauser AG

- Rockwell Automation, Inc.

- Schneider Electric SE