Oil and Gas Fittings Market to Surpass USD 2.1 Billion by 2036

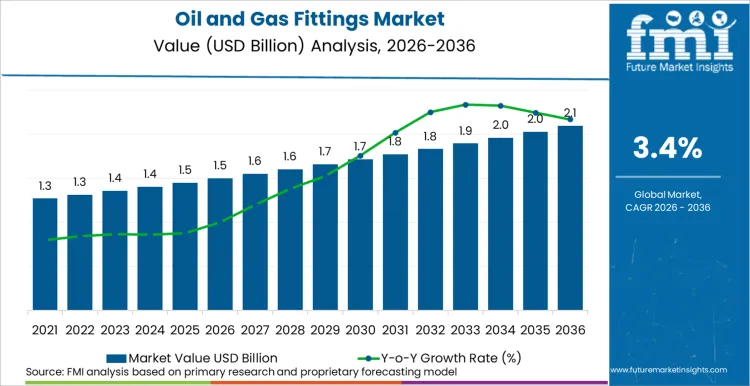

the global oil and gas fittings market is poised for sustained long-term growth as energy companies intensify investments in pipeline modernization, refinery upgrades, midstream infrastructure, and high-performance corrosion-resistant systems. According to the latest analysis by Future Market Insights, the market is projected to grow from USD 1,503.4 million in 2026 to USD 2,100.3 million by 2036, registering a CAGR of 3.4% during the forecast period.

The industry is increasingly shifting toward advanced fittings integrated with digital monitoring technologies, predictive maintenance capabilities, and specialty alloy materials designed to withstand extreme pressure, corrosive environments, and demanding operational conditions across upstream, midstream, and downstream oil and gas operations.

Get detailed market forecasts, competitive benchmarking, and pricing trends: https://www.futuremarketinsights.com/reports/sample/rep-gb-10466

Featured Snippet: Key Market Insights

- Market Value (2025): USD 1,454.0 Million

- Estimated Value (2026): USD 1,503.4 Million

- Forecast Value (2036): USD 2,100.3 Million

- CAGR (2026–2036): 3.4%

- Top Growth Markets: India, Saudi Arabia, China

- Key Drivers: Pipeline integrity programs, refinery modernization, specialty alloy adoption, IoT-enabled fittings

- Core Product Types: Flanges, elbows, tees, reducers, couplings, specialty connectors

Infrastructure Modernization Driving Long-Term Demand

The oil and gas fittings market is witnessing steady infrastructure-led expansion driven by rising investments in pipeline networks, refinery turnaround projects, petrochemical capacity additions, and exploration activities across emerging economies.

Fittings play a critical role in ensuring leak-proof, corrosion-resistant, and high-pressure connections across oil and gas transportation and processing infrastructure. As energy companies prioritize operational reliability and regulatory compliance, demand for advanced fittings manufactured from stainless steel, duplex alloys, and corrosion-resistant specialty materials continues to grow.

Digital twin and IoT-enabled fittings are emerging as a premium market segment, with predictive maintenance capabilities capable of reducing emergency repair costs by nearly 25%.

Key Market Drivers Accelerating Growth

Rising Exploration and Production Investments

Growing upstream investments in shale, offshore, and deepwater exploration are increasing demand for fittings capable of handling extreme temperatures and ultra-high-pressure operations.

Large-scale projects such as Chevron’s Anchor development in the Gulf of Mexico are reinforcing the need for advanced fittings engineered for 20,000 psi operational environments.

Expansion of Midstream Infrastructure

Rapid investments in:

- Cross-border pipeline projects

- LNG transportation infrastructure

- Storage facilities

- Refinery integration systems

are significantly boosting demand for durable and leak-proof fittings.

The midstream segment is expected to remain the largest operational category, accounting for more than 42% market share by 2036.

Adoption of Advanced Materials

Manufacturers are increasingly deploying:

- Duplex stainless steel

- Inconel alloys

- Corrosion-resistant composites

- Super duplex materials

to enhance system durability, improve corrosion resistance, and minimize maintenance costs in harsh offshore and subsea environments.

Regional Market Insights

India: Fastest-Growing Market

India is projected to emerge as one of the fastest-growing oil and gas fittings markets, supported by the government’s ambitious plan to double oil and gas exploration areas to 0.5 million square kilometres.

The country is expected to register a CAGR of approximately 4.5% through 2036, driven by expanding refinery infrastructure and pipeline development projects.

Saudi Arabia

Saudi Arabia continues strengthening its global energy infrastructure through downstream diversification and shale gas expansion initiatives under Vision 2030.

Major investments in the Jafurah shale gas project and refinery integration programs are generating robust demand for high-specification alloy fittings.

United States

The United States market remains driven by:

- Pipeline integrity programs

- Refinery modernization projects

- Shale exploration investments

- Replacement demand for aging infrastructure

Growing deployment of corrosion-resistant and digitally monitored fittings is further enhancing infrastructure reliability.

China

China is witnessing rising demand for advanced fittings as the country expands natural gas infrastructure and petrochemical production capacity.

Natural gas production growth and annual infrastructure investments exceeding USD 14 billion are expected to accelerate long-term market expansion.

Technology Trends Reshaping the Industry

The oil and gas fittings sector is undergoing rapid technological transformation through:

- IoT-enabled smart fittings

- Digital twin integration

- Real-time pipeline monitoring systems

- Predictive maintenance analytics

- Sensor-embedded fittings

- Lightweight high-strength materials

These innovations are improving operational safety, reducing maintenance downtime, and extending pipeline lifecycle performance.

Specialty Alloy Segment Gains Momentum

The market is increasingly bifurcated between commodity-grade carbon steel fittings and premium specialty alloy solutions.

According to industry analysts:

- Commodity carbon steel fittings typically generate margins between 15–20%

- Duplex stainless steel and Inconel fittings can achieve margins above 40%

Demand for specialty alloys is especially strong in sour gas, offshore, high-temperature, and subsea applications.

Supply Chain and Compliance Challenges

Specialty Alloy Supply Constraints

The market faces sourcing challenges due to limited global mill capacity for nickel alloys and duplex stainless steel materials. Rising project activity can extend fitting lead times from 8–12 weeks to over 20 weeks.

Increasing Regulatory Requirements

Post-Macondo regulations and EU PED compliance standards are intensifying requirements for:

- Full material traceability

- Digital certification systems

- Third-party inspection accreditation

- EPC-approved vendor qualifications

Manufacturers investing in digital traceability systems are expected to gain competitive advantages.

Category-Wise Insights

Stainless Steel Segment Leads Market Share

Stainless steel remains the dominant material category due to:

- Superior corrosion resistance

- High mechanical strength

- Reliability in offshore and subsea applications

- Long operational lifespan

The segment is projected to account for approximately 22.8% market share by 2036.

Midstream Operations Dominate Demand

The midstream sector continues to lead market consumption due to rapid expansion of:

- Pipeline infrastructure

- Storage facilities

- LNG transportation systems

- Cross-border energy projects

The segment is projected to account for 42.1% market share by 2036.

Competitive Landscape

The oil and gas fittings market remains moderately consolidated, with global manufacturers focusing on advanced material innovation, EPC partnerships, and smart infrastructure integration.

Leading Market Participants

- Anvil International

- AVK UK Ltd

- B.O.P Products LLC.

- Bonney Forge Corporation

- FitTech Industries Pvt. Ltd.

- Gelbach UK Ltd

- Grupo Cuñado

- Hy-Lok USA, Inc.

- ICARUS SA

These companies are actively investing in corrosion-resistant technologies, digital monitoring systems, and EPC-approved certifications to strengthen their market position.