Sustainable Plastics Revolution Accelerates Growth in the Global Bio-Ethanol to Ethylene Market through 2034

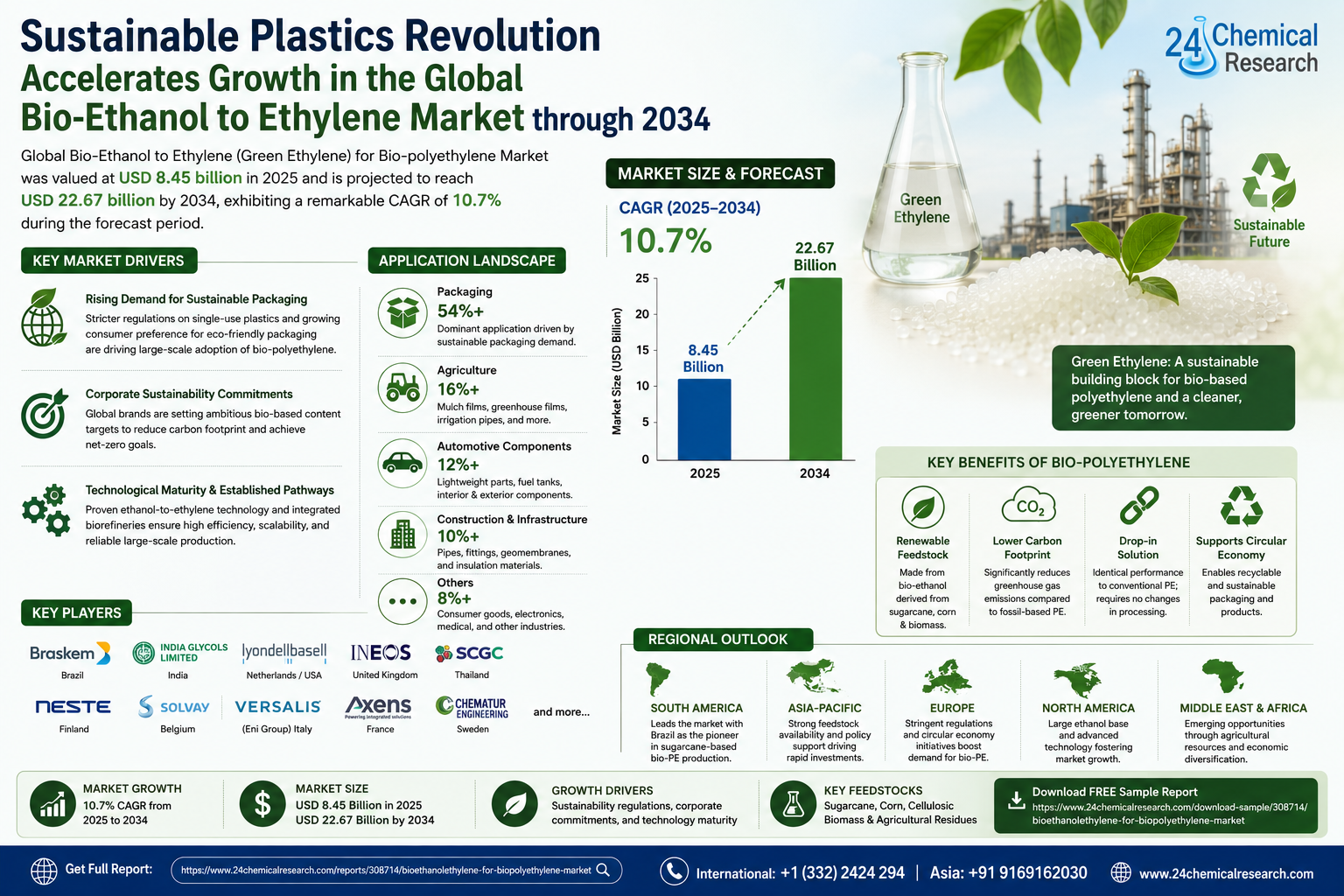

Global Bio-Ethanol to Ethylene (Green Ethylene) for Bio-polyethylene Market was valued at USD 8.45 billion in 2025 and is projected to reach USD 22.67 billion by 2034, exhibiting a remarkable CAGR of 10.7% during the forecast period.

Bio-ethanol to ethylene, commonly referred to as green ethylene, is produced through the catalytic dehydration of bio-ethanol derived from renewable feedstocks such as sugarcane, corn, and cellulosic biomass. This green ethylene serves as a bio-based monomer for the production of bio-polyethylene (bio-PE), a sustainable alternative to conventional fossil-fuel-derived polyethylene. The process encompasses fermentation of biomass to ethanol, followed by dehydration over alumina-based catalysts to yield high-purity ethylene, which is subsequently polymerized into bio-based high-density polyethylene (bio-HDPE) and bio-based low-density polyethylene (bio-LDPE).

Get Full Report Here: https://www.24chemicalresearch.com/reports/308714/bioethanolethylene-for-biopolyethylene-market

Market Dynamics:

The market's trajectory is shaped by a complex interplay of powerful growth drivers, significant restraints that are being actively addressed, and vast, untapped opportunities.

Powerful Market Drivers Propelling Expansion

-

Surging Demand for Sustainable Packaging and Bio-Based Plastics: The global shift toward sustainable packaging is one of the most compelling forces accelerating the bio-ethanol to ethylene market for bio-polyethylene production. Governments across Europe, North America, and Asia-Pacific have enacted increasingly stringent regulations targeting single-use plastics and fossil-fuel-derived polymers, compelling major consumer goods companies, food and beverage manufacturers, and retail giants to reformulate their packaging strategies. Bio-polyethylene, chemically identical to conventional polyethylene but derived from renewable sugarcane ethanol or agricultural feedstocks, offers a drop-in solution that requires no retooling of existing polymer processing infrastructure-a critical commercial advantage that is driving adoption at scale.

-

Corporate Sustainability Commitments and Net-Zero Targets Fueling Bio-PE Procurement: A significant and measurable driver comes from the private sector's binding sustainability commitments. Major multinational brands across fast-moving consumer goods, personal care, and industrial packaging sectors have set formal targets to incorporate recycled or bio-based content into their packaging portfolios. Bio-polyethylene derived from green ethylene carries a substantially lower carbon footprint compared to petroleum-based polyethylene, with lifecycle assessments consistently demonstrating greenhouse gas savings. This carbon reduction profile directly supports scope 3 emissions reduction goals, making bio-PE procurement a strategic lever for corporations navigating increasingly rigorous environmental, social, and governance reporting frameworks.

-

Technological Maturity and Established Production Pathways: The commercial-scale production pathway from bio-ethanol to ethylene is well-established and technically mature. The catalytic dehydration of ethanol to ethylene operates at high conversion efficiencies, and integrated biorefinery models have demonstrated reliable, large-scale output for years. This technological readiness, combined with the availability of competitively priced bio-ethanol, provides a solid commercial foundation. As more regional bio-ethanol production hubs emerge using agricultural residues and second-generation feedstocks, the supply base for green ethylene is expected to broaden significantly, reducing geographic concentration risk and supporting market growth.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/308714/bioethanolethylene-for-biopolyethylene-market

Significant Market Restraints Challenging Adoption

Despite its promise, the market faces hurdles that must be overcome to achieve universal adoption.

-

Feedstock Price Volatility and Agricultural Supply Chain Vulnerabilities: Bio-ethanol production costs are directly tied to the availability and pricing of sugarcane, corn, or lignocellulosic biomass depending on the region, making green ethylene pricing sensitive to seasonal crop cycles, adverse weather events, and competing demand from other sectors. This feedstock price instability creates margin pressure for bio-polyethylene producers and complicates long-term offtake negotiations with downstream converters and brand owners who require pricing predictability for multi-year contracts.

-

Cost Competitiveness Against Fossil-Fuel-Derived Polyethylene: Green ethylene and bio-polyethylene currently carry a price premium over their petroleum-based counterparts. In periods of low crude oil prices, this cost gap widens, undermining the commercial attractiveness of bio-PE for price-sensitive applications where sustainability premiums are not yet supported by consumer or regulatory demand. Achieving cost parity with conventional polyethylene remains a central challenge requiring further scale-up, technology optimization, and supportive policy mechanisms.

Critical Market Challenges Requiring Innovation

The transition from established production to broader industrial-scale manufacturing presents its own set of challenges. While the ethanol-to-ethylene dehydration process is mature, maintaining consistent quality and output at very large volumes remains difficult in newer facilities. Furthermore, ensuring reliable integration into existing polymerization infrastructure can be problematic in some applications. These technical hurdles necessitate continued R&D investments, creating a high barrier to entry for smaller players.

Additionally, the market contends with certification complexity and an evolving supply chain. Producers and customers must navigate multiple certification systems for bio-based content, which increases compliance costs and can slow purchasing decisions. Volatility in agricultural feedstock prices and the added complexity of managing sustainable supply chains compared to traditional materials create economic uncertainty for potential large-scale end-users.

Vast Market Opportunities on the Horizon

-

Expansion into High-Value End-Use Segments: While flexible packaging currently represents the dominant application for bio-polyethylene, substantial growth opportunities exist in higher-value end-use segments including medical, agricultural, and automotive applications. These areas often command significant price premiums where bio-based material credentials and regulatory pressure align, offering certified bio-PE strong potential given its identical functional performance to conventional polyethylene.

-

Growth of Second-Generation Bio-Ethanol Feedstocks and Advanced Biorefinery Integration: The maturation of second-generation bio-ethanol production technologies utilizing agricultural residues presents a transformative opportunity to expand the green ethylene supply base while significantly improving the sustainability profile of bio-polyethylene. Integration with downstream ethanol-to-ethylene dehydration processes could unlock new regional supply chains that are less dependent on first-generation feedstocks and more resilient to competition concerns. This advancement holds the prospect of even stronger environmental benefits.

-

Policy Support and Extended Producer Responsibility Legislation as Commercial Accelerators: Regulatory developments across key markets represent one of the most durable structural opportunities for the bio-ethanol to green ethylene value chain. Packaging regulations, biobased procurement preferences, and carbon pricing mechanisms are creating legislated demand signals that reduce commercial uncertainty for long-term capital investment in bio-PE production capacity, systematically supporting the shift toward green ethylene as a compelling feedstock choice for polymer producers globally.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market is segmented into High-Density Bio-Polyethylene (HDPE), Low-Density Bio-Polyethylene (LDPE), Linear Low-Density Bio-Polyethylene (LLDPE), and others. High-Density Bio-Polyethylene (HDPE) currently leads the market, favored for its rigidity, chemical resistance, and structural durability. Derived from green ethylene, HDPE is increasingly favored by manufacturers seeking drop-in replacements for conventional polymers. LDPE and LLDPE are gaining traction in film and flexible packaging applications where flexibility and processability are critical. As the bio-ethanol supply chain matures, all resin types are expected to benefit from improved feedstock availability.

By Application:

Application segments include Packaging, Agriculture, Automotive Components, Construction & Infrastructure, and others. The Packaging segment currently dominates, driven by intensifying regulatory scrutiny on single-use plastics and growing consumer demand for environmentally responsible solutions. Brand owners across food and beverage, personal care, and consumer goods sectors are committing to bio-based material targets. The agriculture and automotive segments are expected to exhibit strong growth rates in the coming years as lightweighting and sustainability trends advance.

By End-User Industry:

The end-user landscape includes Food & Beverage Industry, Personal Care & Cosmetics, Agriculture & Horticulture, Industrial Manufacturing, and Retail & Consumer Goods. The Food & Beverage industry accounts for the major share, leveraging bio-polyethylene for sustainable packaging to meet consumer and regulatory expectations. The Personal Care and Agriculture sectors are rapidly emerging as key growth end-users, reflecting broader trends in eco-friendly materials and circular economy initiatives.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/308714/bioethanolethylene-for-biopolyethylene-market

Competitive Landscape:

The global Bio-Ethanol to Ethylene (Green Ethylene) for Bio-polyethylene market is semi-consolidated and characterized by intense competition and rapid innovation. The top three companies—Braskem S.A. (Brazil), India Glycols Limited (India), and LyondellBasell Industries—collectively command a leading position in the market. Their dominance is underpinned by extensive production capabilities, vertically integrated operations, and established global distribution networks.

List of Key Bio-Ethanol to Ethylene (Green Ethylene) for Bio-polyethylene Companies Profiled:

-

Braskem S.A. (Brazil)

-

India Glycols Limited (IGL) (India)

-

LyondellBasell Industries (Netherlands / USA)

-

INEOS Group (United Kingdom)

-

SCG Chemicals Co., Ltd. (Thailand)

-

Neste Oyj (Finland)

-

Solvay S.A. (Belgium)

-

Versalis S.p.A. (Eni Group) (Italy)

-

Axens S.A. (France)

-

Chematur Engineering AB (Sweden)

The competitive strategy is overwhelmingly focused on R&D to enhance product quality and reduce costs, alongside forming strategic vertical partnerships with end-user companies to co-develop and validate new applications, thereby securing future demand.

Regional Analysis: A Global Footprint with Distinct Leaders

-

South America: Holds a uniquely important position, led by Brazil as the origin of the world's first and largest commercial bio-polyethylene production based on sugarcane-derived bio-ethanol. The country's integrated sugarcane-to-polymer value chain is recognized globally as a benchmark for commercial viability in this space, with abundant, cost-competitive feedstock and established export markets.

-

Asia-Pacific & Europe: Together they form a powerful secondary bloc. Asia-Pacific benefits from robust agricultural feedstock availability and policy support in countries like India, Thailand, and China. Europe's strength is driven by stringent sustainability regulations and circular economy initiatives that accelerate demand for bio-based materials. Both regions are seeing growing investments in bio-ethanol dehydration and bio-polyethylene capacity.

-

North America, Middle East & Africa: These regions represent emerging frontiers of the market. North America leverages its large corn-based ethanol industry and advanced technology infrastructure, while the Middle East and Africa hold long-term potential through agricultural resources and economic diversification strategies, though infrastructure development remains key to unlocking growth.

Get Full Report Here: https://www.24chemicalresearch.com/reports/308714/bioethanolethylene-for-biopolyethylene-market

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/308714/bioethanolethylene-for-biopolyethylene-market

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

-

Plant-level capacity tracking

-

Real-time price monitoring

-

Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/