Smart Meter Data Management Market Share Size and Outlook 2035

The global smart meter data management (SMDM) market size is moving beyond its early deployment cycle into a more consequential phase—where the value lies not in collecting data, but in interpreting and monetizing it. As utilities worldwide accelerate digital grid transformation, the ability to process, secure, and act on vast streams of real-time consumption data is becoming a defining capability. What began as an infrastructure upgrade is now evolving into a data-driven operating model for the energy sector.

With regulatory mandates, decarbonization goals, and electrification trends converging, SMDM platforms are increasingly positioned at the core of utility strategy—linking operational efficiency, customer engagement, and grid resilience.

Quick Stats: Smart Meter Data Management Market

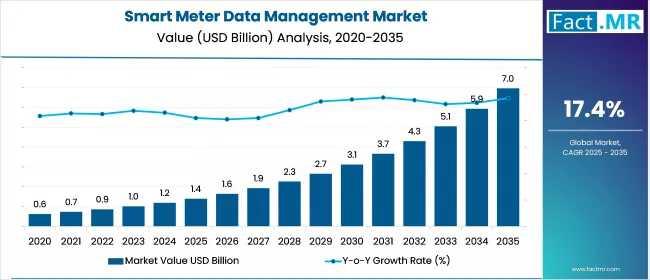

- Market Size (2025): USD 1.4 billion

- Projected Market Size (2035): USD 7.0 billion

- CAGR (2025–2035): 17.4%

- Key Segment Leader: Software-based platforms

- Dominant Deployment Mode: On-premises (with rising cloud adoption)

- High-Growth Markets: China (18.3%), Japan (17.6%), United States (16.1%)

Market Size and Forecast: From Infrastructure to Intelligence

The SMDM market is projected to grow fivefold over the next decade, reaching USD 7.0 billion by 2035. Early growth has been driven by large-scale smart meter rollouts across electricity, gas, and water networks. By 2029, the market is expected to surpass USD 3 billion as utilities scale advanced metering infrastructure (AMI) deployments.

However, the next phase of growth will be structurally different. Spending is increasingly tied to analytics capabilities, system integration, and real-time decision-making, rather than meter deployment alone. By 2030, utilities are expected to shift focus toward extracting value from data—enabling predictive load balancing, automated demand response, and decentralized energy trading models.

Growth Drivers: Policy, Electrification, and Data Volume

Three structural forces are shaping demand:

1. Global Smart Meter Rollouts

Governments and utilities are deploying millions of smart meters to modernize aging infrastructure, reduce losses, and improve billing accuracy. Each deployment generates continuous streams of granular consumption data, requiring robust management systems.

2. Grid Modernization and Energy Transition

The integration of renewable energy sources and distributed energy resources (DERs) demands a more dynamic grid. SMDM platforms enable bidirectional energy flows, support demand response programs, and improve outage management.

3. Data-Driven Utility Operations

Utilities are increasingly leveraging meter data for forecasting, customer segmentation, and operational optimization. This shift toward analytics-led decision-making is expanding the role of SMDM from backend infrastructure to strategic asset.

Challenges: Cost, Complexity, and Cybersecurity

Despite strong momentum, the market faces several structural constraints:

- High Upfront Investment: Full-scale AMI and SMDM deployment requires significant capital, particularly for smaller utilities or developing markets.

- Interoperability Issues: Integrating legacy systems with modern data platforms remains technically complex and resource-intensive.

- Cybersecurity and Data Privacy Risks: Smart meters generate sensitive consumption data, raising concerns around breaches, compliance (e.g., GDPR, CCPA), and public trust.

- Delayed ROI Realization: Benefits such as efficiency gains and loss reduction often materialize over time, complicating investment justification.

These challenges are shaping procurement decisions, with utilities prioritizing scalability, compliance, and long-term cost efficiency.

Opportunities: AI, Cloud, and New Revenue Models

The next wave of growth is being driven by emerging capabilities:

- AI-Driven Analytics: Predictive maintenance, load forecasting, and anomaly detection are unlocking operational efficiencies.

- Cloud and Edge Integration: Hybrid architectures reduce latency and improve scalability, particularly for real-time grid management.

- Dynamic Pricing and Energy Services: Utilities are beginning to monetize data through time-of-use pricing, personalized insights, and energy optimization services.

- Decentralized Energy Systems: SMDM platforms are becoming critical for managing distributed generation and peer-to-peer energy trading.

These developments are repositioning utilities from energy suppliers to data-enabled service providers.

Segmentation Insights: Software and Electric Meters Lead

By Component:

Software dominates the market, reflecting its central role in data ingestion, validation, analytics, and integration with billing and customer systems. Increasing incorporation of AI/ML capabilities is reinforcing this leadership.

By Deployment Mode:

On-premises solutions currently lead, driven by security, regulatory compliance, and legacy infrastructure investments. However, cloud adoption is accelerating due to scalability and lower upfront costs.

By Application:

Electric meters account for the largest share, given their widespread global deployment and critical role in grid operations. Gas and water metering are expanding but remain secondary in scale.

Regional Analysis: Diverging Paths, Converging Goals

North America:

A mature yet evolving market, led by the United States. Growth is driven by grid resilience initiatives, renewable integration, and advanced analytics adoption. Cloud-based SMDM platforms are gaining traction.

Europe:

Regulatory alignment and decarbonization goals underpin demand. Countries like the UK, France, and Italy have completed large-scale deployments, shifting focus to optimization and energy efficiency.

Asia-Pacific:

The fastest-growing region, led by China and India. Massive smart meter rollouts and smart city initiatives are driving demand for scalable data management systems.

- China (18.3% CAGR): Government-led infrastructure expansion and domestic innovation in big data analytics.

- Japan (17.6% CAGR): Focus on energy conservation, grid stability, and aging infrastructure modernization.

Latin America & MEA:

Emerging markets with steady growth, driven by urbanization, energy demand, and early-stage smart grid investments.

Competitive Landscape: Platform Depth and Ecosystem Partnerships

The SMDM market is characterized by a mix of global industrial players and specialized technology providers. Key companies include ABB, Siemens, Honeywell, Itron, Eaton, and Aclara Technologies.

Competition is increasingly defined by:

- End-to-end platform capabilities (data lifecycle management, analytics, integration)

- Cybersecurity and compliance frameworks

- Partnership ecosystems with cloud providers, telecom operators, and system integrators

- M&A activity, as larger firms acquire niche analytics and AI capabilities

Vendors that can combine scalability with regulatory compliance and advanced analytics are gaining strategic advantage.

Strategic Implications for Decision-Makers

For utilities, investors, and technology providers, the market signals several priorities:

- Shift investment focus from hardware to analytics and integration

- Adopt hybrid cloud architectures to balance scalability and compliance

- Strengthen cybersecurity frameworks as data volumes and risks increase

- Build partnerships across the energy-tech ecosystem

- Prepare for new revenue models based on data monetization and customer engagement

Future Outlook: From Metering to Market Intelligence

By 2035, smart meter data management will no longer be viewed as a supporting system—it will be a core operational platform. Utilities that successfully transition from data collection to insight generation will be better positioned to manage decentralized grids, integrate renewables, and engage customers in more dynamic ways.

As electrification accelerates and energy systems become more complex, the competitive edge will increasingly depend on how effectively organizations can convert data into decisions. In that context, SMDM is not just an IT investment—it is a strategic foundation for the next generation of energy infrastructure.

Executive Takeaways

- The SMDM market is set to grow from USD 1.4 billion in 2025 to USD 7.0 billion by 2035, driven by smart grid expansion and data-centric utility models.

- Growth is shifting from infrastructure deployment to analytics, AI, and real-time decision-making capabilities.

- Cybersecurity, interoperability, and ROI timelines remain key barriers.

- Asia-Pacific leads growth, while North America and Europe focus on optimization and advanced services.

- Competitive advantage will hinge on platform depth, ecosystem partnerships, and the ability to enable data-driven energy services.

For executives, the message is clear: the value of smart metering lies not in the meter itself, but in the intelligence extracted from it.

About Fact.MR

Fact.MR is a global market research and consulting firm, trusted by Fortune 500 companies and emerging businesses for reliable insights and strategic intelligence. With a presence across the U.S., UK, India, and Dubai, we deliver data-driven research and tailored consulting solutions across 30+ industries and 1,000+ markets. Backed by deep expertise and advanced analytics, Fact.MR helps organizations uncover opportunities, reduce risks, and make informed decisions for sustainable growth.

- Contact Us -

11140 Rockville Pike, Suite 400, Rockville,

MD 20852, United States

Tel: +1 (628) 251-1583 | sales@factmr.com