Energy Intelligence Solution Market Size Growth Drivers and Outlook

The energy intelligence solution market size is rapidly transitioning from a niche operational tool to a strategic enterprise platform, driven by regulatory pressure, decarbonization mandates, and increasingly complex energy systems. What began as basic energy monitoring software has evolved into AI-powered platforms that integrate real-time analytics, carbon accounting, and demand response optimization across buildings, factories, and utility networks. For C-level executives and investors, energy intelligence is no longer a sustainability add-on—it is becoming a core layer of digital infrastructure.

Quick Stats Snapshot

- Market value (2025): USD 7.9 billion

- Top segment: Energy Management Systems (~34% share)

- Leading deployment model: Cloud-based platforms

- Largest end-use segment: Industrial facilities (~20% revenue share)

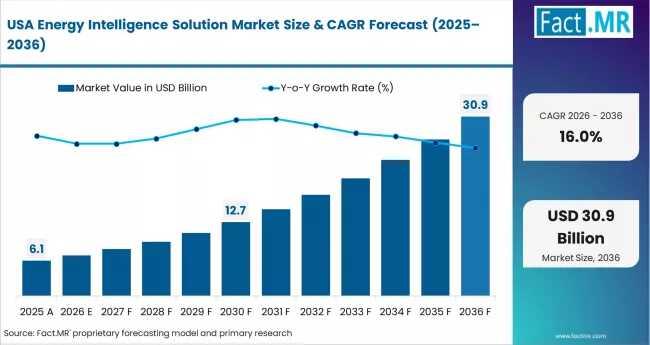

- Top growth markets (CAGR 2026–2036): India (18.0%), China (17.8%), Germany (17.2%), Saudi Arabia (16.3%), U.S. (16.0%)

Market Size and Forecast: From Monitoring Tools to Enterprise Intelligence Layer

Valued at USD 7.9 billion in 2025, the energy intelligence solution market is projected to expand at a high double-digit CAGR through 2036. Growth is being fueled not just by rising adoption, but by increasing contract sizes and longer enterprise agreements, as organizations integrate energy intelligence into broader ESG, digital transformation, and operational efficiency strategies.

The market’s evolution reflects a shift from standalone energy dashboards to integrated AI-driven platforms capable of managing energy consumption, forecasting demand, optimizing costs, and ensuring regulatory compliance in real time.

Growth Drivers: Regulation, AI Optimization, and Smart Infrastructure

- Regulatory Compliance Becomes Non-Negotiable

Global regulations such as the EU’s Corporate Sustainability Reporting Directive (CSRD) and climate disclosure requirements from the U.S. Securities and Exchange Commission are forcing enterprises to adopt auditable, data-driven energy reporting systems. These mandates are transforming energy intelligence from optional to essential. - AI-Driven Energy Optimization

Modern platforms are leveraging machine learning to predict energy demand, optimize load distribution, and reduce waste. This is particularly critical as renewable energy sources introduce variability into grid systems. - Smart City and Grid Modernization Investments

Large-scale infrastructure programs—from India’s utility reforms to Saudi Arabia’s Vision 2030—are accelerating deployment of smart meters, demand response systems, and building energy management platforms.

Challenges: Data Complexity, Integration Costs, and Regulatory Fragmentation

Despite strong tailwinds, adoption is not frictionless:

- Integration with legacy systems remains costly and time-intensive

- Data standardization issues complicate cross-site energy analytics

- Fragmented global regulations require localized platform customization

- Cybersecurity and data sovereignty concerns affect cloud adoption in sensitive sectors

These barriers are particularly relevant for multinational enterprises operating across multiple regulatory environments.

Opportunities: Convergence of Energy, Carbon, and Digital Intelligence

The market is entering a phase where energy intelligence platforms are becoming multi-functional enterprise systems:

- Carbon accounting integration is enabling real-time emissions tracking alongside energy data

- Demand response monetization allows companies to participate in grid balancing markets

- Integration with IoT ecosystems is expanding visibility across assets and operations

- SaaS-based delivery models are lowering entry barriers for mid-sized enterprises

A notable shift is the convergence of energy management with financial and ESG reporting systems, positioning these platforms as decision-making tools rather than operational utilities.

Segmentation Insights: EMS Dominance, Cloud Acceleration

By Solution

Energy Management Systems (EMS) lead the market with approximately 34% share, driven by mandatory energy audits and compliance requirements across industrial and commercial sectors.

By Deployment

Cloud-based solutions dominate due to scalability, remote monitoring capabilities, and lower upfront costs. However, hybrid models are gaining traction where data sovereignty is a concern.

By End Use

Industrial facilities represent the largest revenue segment, reflecting high energy consumption levels and stricter compliance obligations. Commercial real estate and utilities are also significant adopters.

Regional Analysis: Asia Pacific Leads Growth, Europe Drives Policy Adoption

Asia Pacific is the fastest-growing region, anchored by regulatory expansion and industrial demand:

- India (18.0% CAGR): Growth driven by BEE Perform Achieve Trade (PAT) scheme expansion and utility modernization programs

- China (17.8% CAGR): Carbon trading expansion and green building mandates accelerating adoption

Europe remains the most policy-driven market:

- Strict compliance frameworks such as CSRD are mandating enterprise-wide energy reporting

- Countries like Germany are enforcing energy management system adoption in high-consumption industries

Middle East is emerging as a strategic growth region:

- Saudi Arabia’s Vision 2030 and smart city projects are creating demand for integrated building energy systems

North America leads in revenue:

- Strong ESG regulations and grid modernization funding are driving enterprise platform adoption

Competitive Landscape: Platform Integration Defines Market Leadership

The market is moderately consolidated at the top, with large technology providers competing on platform depth, integration capability, and ecosystem reach rather than price alone.

- Schneider Electric leads with its EcoStruxure platform, managing energy data across hundreds of thousands of sites globally

- Siemens AG is advancing AI-enabled building and industrial energy systems through Desigo CC and MindSphere

- Honeywell International leverages its installed base with AI-driven optimization via Honeywell Forge

- ABB Ltd and Emerson Electric are strengthening industrial energy management offerings

- IBM Corporation and General Electric (GE Vernova) are integrating analytics and grid intelligence capabilities

Smaller vendors remain relevant in niche applications but face increasing pressure as large players expand through acquisitions and platform integration.

Strategic Implications: Where Executives Should Focus

For Technology Vendors

- Embed CSRD and SEC compliance features into core platforms

- Expand AI-driven optimization and predictive analytics capabilities

- Offer hybrid cloud architectures to address data sovereignty concerns

For Enterprises and Buyers

- Prioritize platforms that integrate energy, carbon, and operational data

- Evaluate vendors based on long-term scalability and regulatory adaptability

- Consider multi-year contracts to lock in pricing and service continuity

For Investors

- Focus on companies with strong SaaS revenue models and recurring contracts

- Track firms aligned with regulatory-driven demand cycles

- Monitor consolidation trends among platform providers

Future Outlook: From Energy Management to Enterprise Intelligence Backbone

Over the next decade, energy intelligence platforms are expected to evolve into core enterprise systems, integrating with ERP, ESG reporting, and operational technology stacks. The convergence of AI, IoT, and carbon accounting will redefine how organizations manage energy—not as a cost center, but as a strategic asset.

As renewable energy penetration increases and grids become more decentralized, the ability to predict, optimize, and monetize energy usage will become a competitive differentiator.

Executive Takeaways

- Energy intelligence is shifting from compliance tool to strategic platform

- Regulatory mandates are the primary catalyst for enterprise adoption

- AI and cloud technologies are redefining platform capabilities and scalability

- Asia Pacific is the fastest-growing region, while Europe leads in regulation-driven demand

- Market leadership will depend on integration depth, data intelligence, and ecosystem partnerships

In an environment defined by decarbonization and digital transformation, energy intelligence solutions are no longer optional—they are becoming essential infrastructure for resilient, compliant, and efficient enterprises.

About Fact.MR

Fact.MR is a global market research and consulting firm, trusted by Fortune 500 companies and emerging businesses for reliable insights and strategic intelligence. With a presence across the U.S., UK, India, and Dubai, we deliver data-driven research and tailored consulting solutions across 30+ industries and 1,000+ markets. Backed by deep expertise and advanced analytics, Fact.MR helps organizations uncover opportunities, reduce risks, and make informed decisions for sustainable growth.

- Contact Us -

11140 Rockville Pike, Suite 400, Rockville,

MD 20852, United States

Tel: +1 (628) 251-1583 | sales@factmr.com