Electric Vehicle Battery Market Size Expansion Trends and Outlook 2035

The global electric vehicle (EV) battery industry is moving from a phase of rapid adoption into a more strategic era shaped by industrial policy, mineral security, manufacturing localization, and technological differentiation. What was once primarily a supplier market serving early EV growth is becoming a central pillar of automotive competitiveness and energy transition planning.

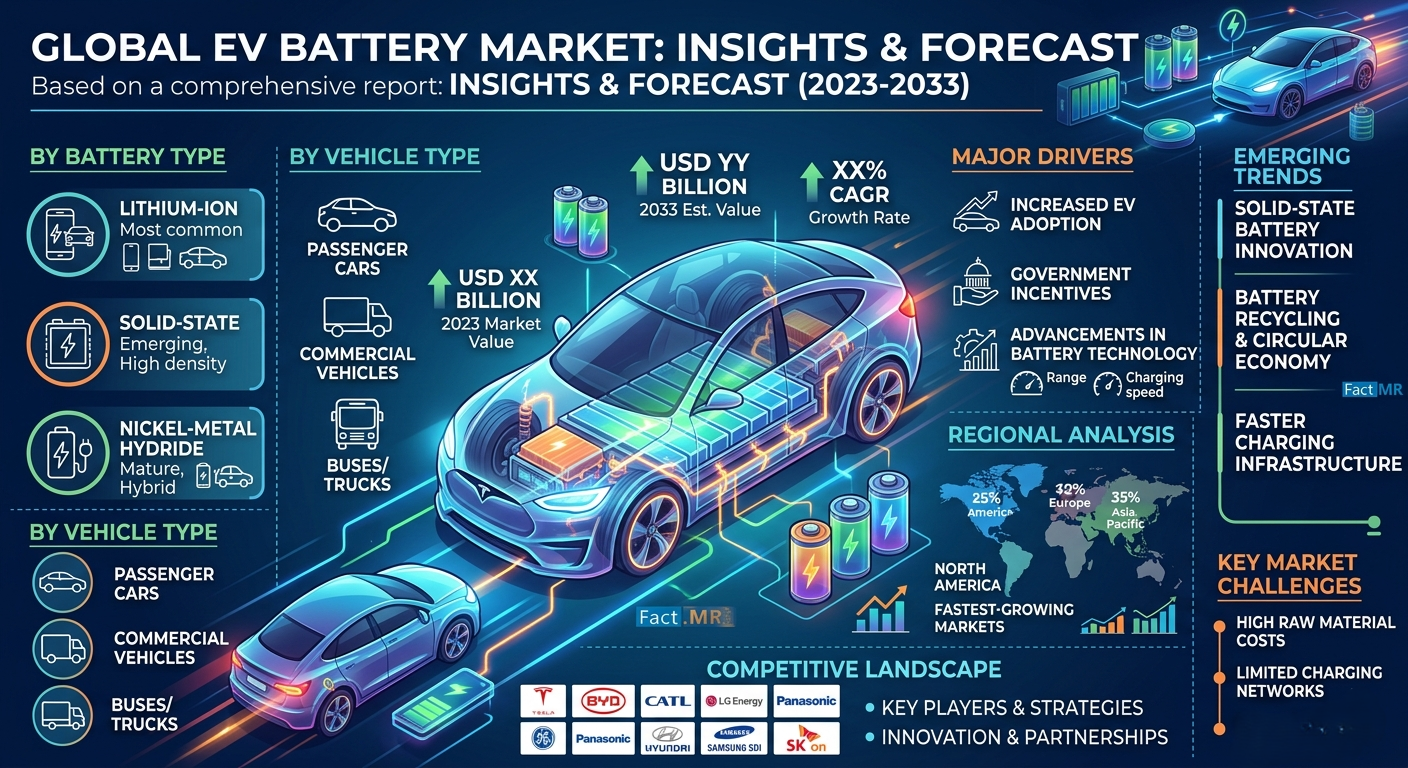

Electric Vehicle Battery Market Size Between 2025 and 2035, the EV battery market is projected to expand from USD 66.7 billion to USD 256.0 billion, reflecting a compound annual growth rate (CAGR) of 14.4%. The scale of this expansion signals more than rising EV sales—it reflects a structural transformation in transportation, energy storage, and industrial manufacturing worldwide.

As governments tighten emissions regulations, automakers accelerate electrification programs, and utilities integrate renewable energy systems, batteries are emerging as one of the most strategically important technologies in the global economy. Industry leaders are no longer competing solely on vehicle performance; increasingly, they are competing on battery chemistry, sourcing resilience, charging efficiency, and lifecycle sustainability.

Quick Stats: Electric Vehicle Battery Market

- Market Size (2025): USD 66.7 Billion

- Forecast Value (2035): USD 256.0 Billion

- CAGR (2025–2035): 14.4%

- Leading Chemistry Segment: NMC/High-Nickel & LFP Blends

- Largest Application Segment: Passenger EVs

- Fastest-Growing Regions: North America, Asia Pacific

- Key Industry Participants: CATL, BYD, Panasonic, LG Energy Solution, Samsung SDI

Battery Manufacturing Becomes a Strategic Industry

The next decade will likely redefine how nations approach automotive manufacturing and energy independence. Batteries are increasingly viewed as strategic infrastructure assets rather than automotive components alone.

The first growth phase between 2025 and 2030 is expected to add more than USD 63 billion in market value. During this period, automakers and battery suppliers are expected to prioritize scaling production capacity, securing lithium and nickel supply agreements, and improving manufacturing efficiency.

The second phase, from 2030 to 2035, is forecast to contribute an additional USD 126 billion in market expansion. This period will likely be characterized by battery ecosystem maturity, including recycling networks, second-life applications, solid-state advancements, and deeper integration with intelligent vehicle systems.

For executives and investors, the implication is clear: the competitive landscape will increasingly favor companies capable of controlling battery supply chains end-to-end—from raw material sourcing to advanced chemistry development and localized production.

Why Demand for EV Batteries Continues to Accelerate

Several macroeconomic and industrial trends are reinforcing long-term demand.

Electrification Mandates and Climate Policy

Governments across North America, Europe, and parts of Asia continue to introduce aggressive emissions targets and internal combustion engine phase-out plans. These policies are directly increasing battery demand across passenger and commercial vehicle categories.

In Europe, stricter emissions regulations and carbon reduction mandates are accelerating EV production investments. In the United States, federal incentives tied to domestic manufacturing and sourcing requirements are reshaping battery procurement strategies.

Declining Battery Costs

Battery pack prices have fallen significantly over the past decade, making EVs increasingly cost-competitive with conventional vehicles. Although raw material volatility remains a challenge, advances in manufacturing scale and chemistry optimization continue to improve economics.

Lithium iron phosphate (LFP) batteries, in particular, are gaining traction because of their lower cost profile and improved thermal stability.

Expansion of Charging Infrastructure

Rapid deployment of public charging networks is reducing consumer adoption barriers. At the same time, improvements in charging speed and energy density are helping EVs achieve greater mainstream acceptance.

Energy Storage Convergence

Battery manufacturers are increasingly serving dual markets: electric mobility and stationary energy storage systems (ESS). As renewable energy adoption rises globally, battery technologies are becoming critical for grid balancing and energy reliability.

This convergence is creating new revenue opportunities for manufacturers capable of supplying both transportation and utility-scale storage applications.

Market Challenges Remain Significant

Despite strong growth momentum, the industry faces structural constraints that could influence pricing, profitability, and supply reliability.

Critical Mineral Dependency

Lithium, nickel, cobalt, and graphite supply chains remain vulnerable to geopolitical disruptions and resource concentration risks. Mining bottlenecks and refining limitations continue to create uncertainty for procurement teams and automakers.

China’s dominance in refining and battery processing remains a major concern for Western governments seeking supply diversification.

Battery Degradation and Charging Limitations

Although battery performance continues to improve, concerns around degradation, charging times, and cold-weather efficiency still affect consumer perception and fleet adoption.

Manufacturers are investing heavily in thermal management systems, fast-charging technologies, and advanced battery management software to address these limitations.

Manufacturing Intensity and Capital Requirements

Battery gigafactories require enormous capital investments and highly specialized production expertise. The industry’s rapid expansion is creating pressure on labor availability, energy infrastructure, and manufacturing quality control.

Companies unable to scale production efficiently may struggle to remain competitive as pricing pressure intensifies.

NMC and LFP Chemistries Continue to Lead

Battery chemistry remains one of the industry’s most important strategic battlegrounds.

NMC/High-Nickel and LFP Blends Hold Leading Share

NMC/high-nickel and LFP blend systems account for approximately 46% of the global market. These chemistries are widely adopted because they balance energy density, safety, charging performance, and operational reliability.

High-nickel formulations are particularly important for premium EVs and long-range vehicles, while blended systems help manufacturers optimize performance and cost efficiency.

LFP Batteries Gain Wider Adoption

LFP batteries hold roughly 30% market share and are increasingly favored for mass-market vehicles, commercial fleets, and cost-sensitive applications.

Their advantages include:

- Lower production costs

- Improved thermal safety

- Longer cycle life

- Reduced dependency on cobalt and nickel

As automakers push affordable EV platforms into emerging markets, LFP adoption is expected to rise substantially.

Passenger EVs Remain the Dominant Application Segment

Passenger electric vehicles account for approximately 71% of global EV battery demand.

Consumer demand for sustainable transportation, coupled with expanding model availability across price categories, continues to drive battery consumption in this segment.

Commercial EV adoption is also gaining momentum, particularly in logistics, public transportation, and urban delivery fleets. Fleet operators are increasingly prioritizing electrification to reduce fuel costs and meet emissions targets.

Meanwhile, stationary energy storage systems are emerging as a strategically important secondary market, particularly for utilities integrating renewable power generation.

North America Emerges as a Strategic Growth Hub

While Asia Pacific remains the manufacturing center of the EV battery industry, North America is becoming one of the fastest-growing investment regions.

United States

The U.S. market is projected to grow at a CAGR of 15.8% through 2035. Federal incentives tied to domestic battery manufacturing, EV assembly, and critical mineral sourcing are accelerating investment in gigafactory development.

States such as Michigan, Texas, and California are emerging as key battery production and EV innovation hubs.

Automakers and battery suppliers are increasingly localizing operations to reduce geopolitical exposure and qualify for incentive programs.

Mexico

Mexico is becoming an important regional manufacturing node due to automotive production growth, competitive labor costs, and integration with North American supply chains.

The country’s projected 14.4% CAGR highlights its growing role in EV assembly and battery ecosystem expansion.

Europe Strengthens Regulatory Leadership

Europe’s EV battery market is expected to grow from USD 18.5 billion in 2025 to USD 70.0 billion by 2035.

Germany remains the region’s largest market, supported by its advanced automotive manufacturing base and strong engineering ecosystem. France and the UK continue to invest heavily in electrification and battery innovation programs.

European policymakers are also pushing battery passport regulations, recycling standards, and supply chain traceability requirements that could influence global industry practices.

Asia Pacific Maintains Manufacturing Dominance

Asia Pacific continues to lead global battery production capacity, particularly in China, South Korea, and Japan.

Chinese manufacturers retain strong advantages in scale, raw material processing, and vertical integration. South Korean companies remain highly competitive in premium battery technology and global OEM partnerships.

Japan continues to focus on high-performance battery systems emphasizing durability, energy precision, and advanced chemistry integration.

Competitive Landscape: Scale, Technology, and Integration Define Market Leadership

The EV battery industry remains moderately concentrated, with leading companies controlling a substantial portion of global supply.

Major participants include:

- Contemporary Amperex Technology Co. Limited

- BYD Company Ltd.

- Panasonic Corporation

- LG Energy Solution

- Samsung SDI Co. Ltd.

- SK On

Competition is increasingly centered around:

- Energy density improvements

- Fast-charging capability

- Manufacturing scale

- Supply chain localization

- Software-enabled battery management

- Recycling and sustainability credentials

Strategic partnerships between automakers and battery suppliers are also intensifying, as OEMs seek greater control over long-term battery sourcing and intellectual property.

Strategic Implications for Industry Stakeholders

For Automakers

Battery strategy is becoming inseparable from vehicle strategy. OEMs that secure stable supply agreements and invest in chemistry innovation may achieve stronger pricing power and production resilience.

For Investors

The sector presents long-term growth potential, but capital allocation decisions increasingly depend on manufacturing execution, mineral sourcing stability, and technology differentiation rather than EV demand alone.

For Procurement Leaders

Supply diversification and regional manufacturing partnerships are becoming essential risk-management priorities amid ongoing geopolitical uncertainty.

For Policymakers

Battery production capacity is rapidly becoming a matter of economic competitiveness and industrial sovereignty. Nations investing in domestic battery ecosystems are positioning themselves for long-term automotive and energy leadership.

Future Outlook

The EV battery market is entering a decisive period where growth will be driven not only by rising EV adoption, but also by broader transformations in energy infrastructure, industrial policy, and global trade dynamics.

By 2035, battery technology is expected to become more integrated, intelligent, recyclable, and geographically diversified. Companies that successfully balance scale, sustainability, and technological innovation are likely to shape the next generation of mobility and energy systems.

For decision-makers across automotive, manufacturing, energy, and finance sectors, the next decade will not simply determine who leads the EV market—it may determine who leads the future industrial economy itself.

About Fact.MR

Fact.MR is a global market research and consulting firm, trusted by Fortune 500 companies and emerging businesses for reliable insights and strategic intelligence. With a presence across the U.S., UK, India, and Dubai, we deliver data-driven research and tailored consulting solutions across 30+ industries and 1,000+ markets. Backed by deep expertise and advanced analytics, Fact.MR helps organizations uncover opportunities, reduce risks, and make informed decisions for sustainable growth.

- Contact Us -

11140 Rockville Pike, Suite 400, Rockville,

MD 20852, United States

Tel: +1 (628) 251-1583 | sales@factmr.com