Aluminum Foam Sandwich Panel for Train Flooring Set to Hit USD 342.5 Million by 2034 at 7.0% CAGR

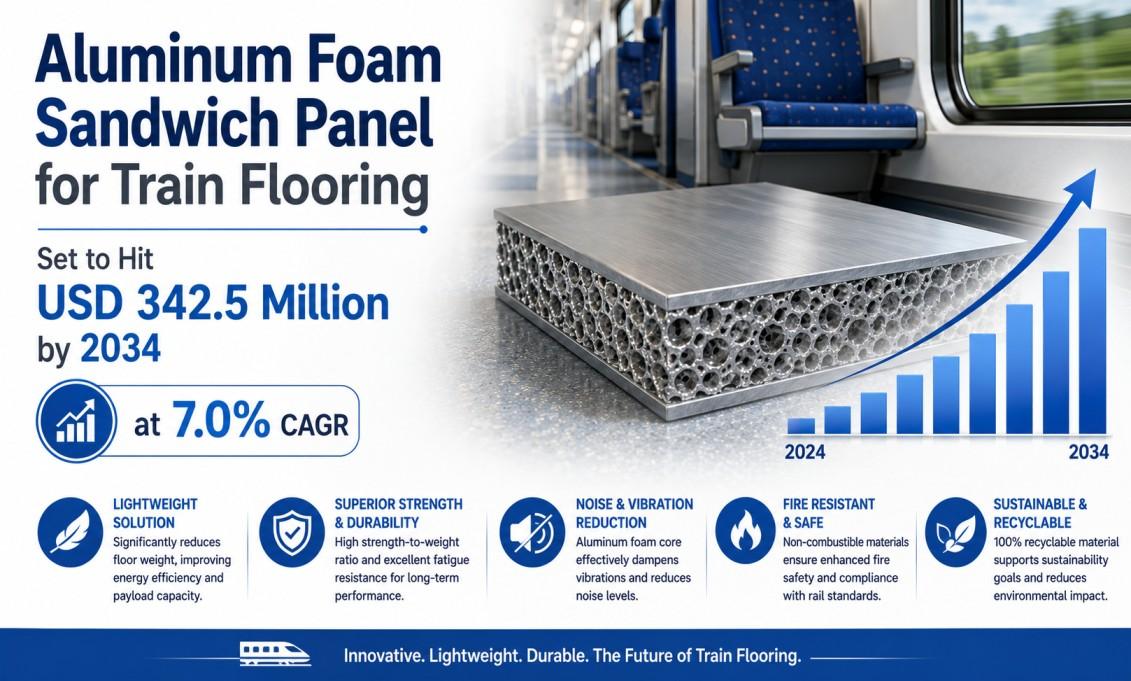

Global Aluminum Foam (Closed Cell) Sandwich Panel for Train Flooring market size was valued at USD 187.4 million in 2025. The market is projected to grow from USD 198.6 million in 2026 to USD 342.5 million by 2034, exhibiting a remarkable CAGR of 7.0% during the forecast period.

Aluminum foam (closed cell) sandwich panels are advanced composite structural materials consisting of two dense aluminum face sheets bonded to a lightweight closed-cell aluminum foam core. This construction delivers an exceptional combination of high stiffness, low weight, superior acoustic damping, and outstanding fire resistance—properties that make these panels particularly well-suited for train flooring applications. The closed-cell structure ensures minimal water absorption and enhanced thermal insulation, while the aluminum composition contributes to the overall durability and longevity of the flooring system. Unlike conventional flooring substrates, the sealed cellular architecture of the foam core provides consistent mechanical performance across a wide range of operating temperatures and load conditions, making it a robust choice for the demanding environment of rail transit interiors.

Get Full Report Here: https://www.24chemicalresearch.com/reports/308945/aluminum-foam-swich-panel-for-train-flooring-market

Market Dynamics:

The market's trajectory is shaped by a complex interplay of powerful growth drivers, significant restraints that are being actively addressed, and vast, untapped opportunities spanning multiple geographies and rail segments.

Powerful Market Drivers Propelling Expansion

-

Expanding Rail Infrastructure Investment Globally Fueling Demand for Advanced Flooring Solutions: Governments and transit authorities across Europe, Asia-Pacific, and North America are committing substantial capital to railway modernization and new rail corridor development. High-speed rail projects, urban metro expansions, and intercity rail upgrades are collectively generating strong procurement demand for lightweight, structurally robust interior components—with train flooring ranking among the most specification-critical elements. Aluminum foam closed cell sandwich panels have emerged as a preferred solution in this context because they simultaneously address weight reduction targets, structural load requirements, and fire safety mandates that conventional flooring materials struggle to meet in combination. The depth and scale of this global infrastructure pipeline represents the single most powerful commercial force driving sustained market expansion through 2034.

-

Stringent Lightweight and Energy Efficiency Standards Pushing Rail OEMs Toward Aluminum Foam Panels: Rail vehicle manufacturers face intensifying regulatory and commercial pressure to reduce overall trainset weight in order to lower energy consumption per passenger-kilometer. Closed cell aluminum foam sandwich panels offer a compelling mass-to-stiffness ratio that outperforms traditional steel or solid aluminum flooring substrates. Because the closed cell foam core traps air within sealed cells, the panel delivers high compressive strength while maintaining a density significantly lower than comparable solid-metal alternatives. This directly translates to measurable reductions in traction energy demand over the operational life of a trainset—a factor that increasingly influences procurement decisions among rail operators facing carbon reduction commitments. Beyond weight, the inherent vibration damping characteristics of closed cell aluminum foam panels contribute to improved passenger comfort, while their superior acoustic insulation performance helps operators comply with interior noise level standards without adding treatment layers that would otherwise offset weight savings.

-

Fire Safety Regulation Tightening Creating Structural Preference for Non-Combustible Flooring Materials: The direction of travel in rail fire safety regulation globally is unmistakably toward more stringent requirements for interior materials, including flooring. Aluminum foam closed cell sandwich panels inherently offer fire resistance characteristics—including low flame spread, limited smoke generation, and absence of halogenated compounds—that align with the requirements of standards such as EN 45545 in Europe and GB/T 29836 in China. As rail operators in markets that have historically applied less rigorous standards begin aligning with these international benchmarks, aluminum foam panels benefit competitively relative to organic-core flooring alternatives. This regulatory tailwind is not a speculative future factor; it is actively reshaping material selection decisions in current procurement cycles across multiple markets, reinforcing demand for aluminum foam solutions at both the newbuild and refurbishment stages of rolling stock programs.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/308945/aluminum-foam-swich-panel-for-train-flooring-market

Significant Market Restraints Challenging Adoption

Despite its clear performance advantages, the market faces meaningful hurdles that must be overcome to achieve broader adoption across all rail tiers and geographies.

-

Entrenched Alternative Materials and Conservative Procurement Specifications Slowing Market Penetration: Rail flooring specifications are historically conservative documents, often anchored to material types—such as marine-grade plywood with aluminum sheeting or glass-fiber reinforced plastic panels—that have decades of field validation behind them. Type approval and homologation processes for new flooring materials in certified rail vehicles are resource-intensive and time-consuming, particularly in regulated markets such as the European Union where EN 45545 fire safety standards and related structural requirements demand extensive testing documentation. For aluminum foam sandwich panels entering a new rail program specification for the first time, this approval burden represents a meaningful commercial restraint, as rail OEMs must absorb qualification costs before series procurement can begin. The result is a slower-than-optimal penetration rate even in markets where the technical case for aluminum foam panels is well established.

-

Raw Material Price Volatility Adding Uncertainty to Panel Pricing Stability: Aluminum commodity prices are subject to fluctuation driven by global energy costs—given the energy-intensive nature of primary aluminum smelting—as well as by geopolitical factors affecting bauxite supply chains and trading conditions. Because closed cell aluminum foam panels are aluminum-intensive by composition, sustained periods of elevated aluminum pricing directly compress panel manufacturer margins or require price adjustments that can disrupt multi-year supply agreements with rail OEMs. This pricing volatility introduces contract negotiation complexity and can make long-term program cost planning more challenging for both panel producers and their rail industry customers, particularly in an environment where infrastructure project budgets are fixed at the time of contract award.

Critical Market Challenges Requiring Innovation

The production of closed cell aluminum foam sandwich panels involves technically demanding processes—including powder metallurgy foaming routes or melt-foaming techniques—that require specialized equipment and process control capabilities not widely available in standard metal fabrication facilities. This manufacturing complexity translates into elevated per-unit costs relative to conventional plywood-core or steel-framed flooring alternatives, which remain entrenched in lower-budget regional and freight rail applications. Rail OEMs supplying cost-sensitive market segments therefore face difficulty justifying the lifecycle cost case for aluminum foam panels when procurement decisions are driven primarily by upfront capital expenditure rather than total cost of ownership.

Furthermore, the global supply of high-quality closed cell aluminum foam panels suitable for rail flooring applications remains concentrated among a relatively small number of specialist producers, primarily located in Europe and select Asian markets. This geographic and supplier concentration introduces procurement risk for rail OEMs and transit authorities seeking assured, high-volume supply. Qualification and certification of alternative suppliers is a lengthy process in the rail sector given the safety-critical nature of floor structures, which further constrains supply chain flexibility and can contribute to lead time volatility during periods of elevated rail infrastructure spending. Additionally, closed cell aluminum foam sandwich panels require specialized repair protocols when damaged in field operations—a complexity that existing rail depot maintenance infrastructure is not always equipped to support, creating tension with lifecycle management requirements over the long operational service life of rolling stock.

Vast Market Opportunities on the Horizon

-

Rising High-Speed Rail and Urban Metro Procurement Pipelines Creating Large-Volume Application Opportunities: The global pipeline of high-speed rail and urban mass transit projects—particularly across India, Southeast Asia, the Middle East, and continental Europe—represents a substantial and growing addressable market for advanced train flooring systems. High-speed trainsets in particular place a premium on lightweight interior structures because mass reduction directly improves operational economics over high-frequency service cycles. As rail authorities in emerging markets develop new rolling stock specifications for these programs, there is a significant opportunity for aluminum foam sandwich panel manufacturers to engage early in the design process and secure specification inclusion before conventional materials become entrenched. This proactive market engagement strategy differs meaningfully from the retrofit-focused opportunity available in mature Western markets, and it carries the potential for long-run, high-volume supply relationships spanning the full production lifetime of newly specified train platforms.

-

Retrofit and Refurbishment Market Offering Near-Term Revenue Potential Alongside Newbuild Programs: Beyond newbuild rolling stock programs, the substantial global fleet of aging rail vehicles undergoing midlife refurbishment presents an accessible near-term market for aluminum foam sandwich panel suppliers. Floor replacement is among the most common refurbishment interventions undertaken during heavy maintenance cycles because train floors accumulate wear, moisture ingress, and structural fatigue over years of intensive passenger service. Specifying aluminum foam panels during refurbishment offers fleet operators an opportunity to simultaneously upgrade fire performance, reduce vehicle mass, and extend service intervals—a compelling multi-benefit value proposition that can be presented independently of the longer design-cycle timeline associated with newbuild program specifications. This makes the refurbishment segment a particularly attractive near-term commercialization pathway for manufacturers seeking revenue opportunities ahead of major newbuild program awards.

-

Strategic Partnerships and Co-Development Agreements Accelerating Specification Adoption: The market is witnessing growing momentum in collaboration between aluminum foam panel manufacturers and major rolling stock OEMs. These partnerships—structured around co-development of application-specific panel configurations, joint qualification testing, and long-term supply commitments—are proving instrumental in shortening the time required to move from material evaluation to series procurement approval. For panel manufacturers, embedding their products within an OEM's standard material library through such alliances effectively reduces competitive exposure across the multi-year production run of each rolling stock platform. For OEMs, these partnerships provide supply certainty and early access to material performance improvements as manufacturers continue to refine their production processes. The expanding number of such collaborative arrangements across Europe and Asia-Pacific signals a maturing commercial ecosystem that should support accelerating market growth through the forecast period.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market is segmented into Single-Skin Aluminum Foam Sandwich Panel, Double-Skin Aluminum Foam Sandwich Panel, Hybrid Composite Aluminum Foam Sandwich Panel, and Customized Thickness Aluminum Foam Sandwich Panel. Double-Skin Aluminum Foam Sandwich Panel holds the leading position in this segment, owing to its superior structural rigidity and enhanced load-bearing characteristics that are critical for high-traffic train flooring environments. The double-skin configuration provides an exceptional balance between mechanical strength and overall weight reduction, making it a preferred choice among rolling stock manufacturers seeking to comply with stringent railway safety and performance standards. Hybrid composite variants are gaining meaningful traction as manufacturers explore multi-material integration to further optimize performance profiles for next-generation rail platforms.

By Application:

Application segments include High-Speed Rail Flooring, Metro and Suburban Rail Flooring, Light Rail and Tram Flooring, Freight and Cargo Train Flooring, and others. High-Speed Rail Flooring emerges as the dominant application segment, driven by the critical demand for lightweight yet structurally robust flooring solutions that directly support energy efficiency goals and aerodynamic performance in high-speed rail systems. Metro and suburban rail flooring represents a rapidly expanding application area, as urban transit authorities worldwide modernize aging fleets and commission new rolling stock with an emphasis on reduced lifecycle maintenance costs and enhanced durability under intensive daily use.

By End User:

The end-user landscape includes Original Equipment Manufacturers (OEMs), Rail Operators and Transit Authorities, and Maintenance, Repair and Overhaul (MRO) Service Providers. Original Equipment Manufacturers (OEMs) constitute the leading end-user segment, as they are the primary integrators of aluminum foam closed-cell sandwich panels during the initial design and fabrication phase of new train carriages and rolling stock. OEMs work in close collaboration with material suppliers to develop customized panel specifications that align with project-specific weight, fire resistance, and structural performance requirements mandated by rail industry standards such as EN 45545 and UIC norms. Rail operators and transit authorities represent a steadily growing end-user base as they pursue fleet refurbishment programs, while MRO providers play an increasingly vital supporting role in ensuring the long-term integrity of installed panels.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/308945/aluminum-foam-swich-panel-for-train-flooring-market

Competitive Landscape:

The global Aluminum Foam (Closed Cell) Sandwich Panel for Train Flooring market is characterized by a relatively concentrated group of specialized manufacturers, predominantly based in Europe and Asia, with a growing presence in North America. The market is semi-consolidated, with leading European firms such as Alulight International GmbH (Austria) and Pohltec Metalfoam GmbH (Germany) holding long-standing supply relationships with major rolling stock manufacturers including Alstom, Siemens Mobility, and Bombardier Transportation (now part of Alstom). Their dominance is underpinned by deep material science capabilities, established certification frameworks compliant with railway standards such as EN 45545, and vertically integrated manufacturing processes that create meaningful barriers to entry for new competitors.

Beyond the established leaders, a number of niche and emerging manufacturers are gaining traction by targeting specific regional rail markets or offering customized panel configurations. Chinese domestic players are increasingly competitive in Asia-Pacific, driven by China's large-scale high-speed rail and metro expansion programs. The competitive strategy across the industry is overwhelmingly focused on R&D investment to improve foam density uniformity, surface finish quality, and panel joining methods, alongside forming strategic vertical partnerships with end-user companies to co-develop and validate new applications, thereby securing future demand across the forecast period.

List of Key Aluminum Foam (Closed Cell) Sandwich Panel for Train Flooring Companies Profiled:

-

Alulight International GmbH (Austria)

-

Pohltec Metalfoam GmbH (Germany)

-

Cymat Technologies Ltd. (Alusion) (Canada)

-

Foamtech Co., Ltd. (South Korea)

-

3A Composites GmbH (Switzerland)

-

Shanxi Putai Aluminum Foam Manufacturing Co., Ltd. (China)

-

ERG Aerospace Corporation (United States)

The competitive environment is further shaped by ongoing R&D investments aimed at improving foam density uniformity, surface finish quality, and panel joining methods to meet the increasingly stringent requirements of next-generation rail vehicle platforms. Manufacturers that demonstrate technology leadership in panel customization—including integration of anti-slip surfaces, embedded insulation layers, and modular sizing configurations—are increasingly gaining preference among major rolling stock manufacturers during the supplier qualification process.

Regional Analysis: A Global Footprint with Distinct Leaders

-

Europe: Stands as the leading region in the aluminum foam closed cell sandwich panel market for train flooring, driven by its long-established and highly advanced rail network infrastructure. Countries such as Germany, France, the United Kingdom, and the Nordic nations have consistently prioritized lightweight, fire-resistant, and thermally efficient materials in rolling stock modernization programs. The European Union's stringent rail safety directives and fire protection standards, including EN 45545, have directly encouraged the adoption of advanced sandwich panel solutions. Furthermore, ongoing investments in cross-border rail corridors, green mobility initiatives, and fleet renewal programs across the continent continue to sustain consistent demand. The presence of leading panel manufacturers within the region further reinforces Europe's dominant market position.

-

Asia-Pacific: Represents the fastest-growing regional market, underpinned by the region's massive and ongoing expansion of rail infrastructure. China, Japan, South Korea, and India are at the forefront of high-speed rail development, urban metro construction, and commuter rail modernization, all of which demand advanced lightweight and structurally robust flooring materials. China's extensive high-speed rail network—the largest globally—drives substantial procurement of innovative materials to meet performance and weight reduction targets. India's ambitious rail electrification and fleet expansion programs further contribute to regional demand, and the growing alignment of regional regulatory standards toward international fire safety norms is supporting broader adoption of certified aluminum foam panel solutions throughout the region.

-

North America, South America, and Middle East & Africa: North America occupies a moderate but steadily developing position, with renewed interest in passenger rail driven by federal investment programs targeting intercity rail corridors and urban transit modernization. South America presents an emerging market characterized by selective but growing investments in urban rail and metro systems across Brazil, Chile, Colombia, and Argentina, though budget constraints and a limited domestic manufacturing base currently constrain penetration. The Middle East and Africa, while nascent in scale, represent a strategically notable region given landmark rail and metro projects in GCC countries such as Saudi Arabia and the United Arab Emirates, where high-specification materials for rolling stock are increasingly demanded under international procurement standards. These regions collectively represent the evolving frontier of the global market, with long-term growth potential that will become increasingly material as infrastructure pipelines progress through development and procurement phases.

Get Full Report Here: https://www.24chemicalresearch.com/reports/308945/aluminum-foam-swich-panel-for-train-flooring-market

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/308945/aluminum-foam-swich-panel-for-train-flooring-market

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

-

Plant-level capacity tracking

-

Real-time price monitoring

-

Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/