Lead Acid Battery Market Forecast 2026–2036: Global Market to Reach USD 58.2 Billion by 2036

The global lead acid battery market is projected to expand steadily over the next decade, increasing from approximately USD 42.8 billion in 2026 to USD 58.2 billion by 2036, registering a CAGR of 3.1%, according to the latest analysis by Future Market Insights (FMI).

Market growth is being shaped by increasing demand for cost-effective and reliable energy storage solutions across automotive, industrial, and backup power applications. Lead acid batteries remain widely used due to their established recycling ecosystem, affordability, and strong compatibility with existing power systems and infrastructure.

Although newer battery technologies such as lithium-ion are gaining attention, lead acid batteries continue to maintain strong demand in automotive starter systems, telecom backup power, and industrial energy storage due to their reliability and well-developed global recycling network. The industry is also evolving with improvements in battery designs such as AGM (Absorbent Glass Mat) and VRLA (Valve-Regulated Lead-Acid) batteries, enhancing performance and reducing maintenance requirements.

Lead Acid Battery Market Snapshot (2026–2036)

-

Market size in 2026: USD 42.8 billion

-

Market size in 2036: USD 58.2 billion

-

CAGR (2026–2036): 3.1%

-

Leading product type: Flooded batteries (~45% share in 2026)

-

Leading application: Transportation (~40% share)

-

Key growth regions: Asia Pacific, North America, Europe

-

Fastest-growing countries: India, China, United States, Japan

Momentum in the Market

Beginning at around USD 42.8 billion in 2026, the lead acid battery market demonstrates steady expansion across the forecast period. The automotive industry continues to represent a major demand driver due to the consistent replacement cycle for vehicle batteries and widespread use in starting, lighting, and ignition (SLI) systems.

Between 2030 and 2036, continued investments in telecom infrastructure, industrial backup power systems, and energy storage solutions are expected to sustain market demand. Increasing adoption of improved battery technologies such as AGM and VRLA batteries further enhances reliability, operational efficiency, and lifecycle performance.

Additionally, the global lead acid battery industry benefits from one of the most mature recycling ecosystems, enabling manufacturers to recover a significant portion of lead materials and reduce environmental impact while maintaining cost competitiveness.

The Reasons Behind the Market's Growth

Demand for lead acid batteries is increasing as industries prioritize reliable and economical energy storage solutions. Their widespread adoption across automotive, industrial, and stationary applications continues to support long-term market stability.

One of the primary growth drivers is the automotive sector, where lead acid batteries remain essential for ignition systems in conventional vehicles and hybrid platforms. Replacement demand from millions of vehicles globally ensures recurring sales.

In addition, expanding telecom networks, data centers, and backup power systems are strengthening demand for stationary lead acid batteries. Industrial sectors rely heavily on these batteries for uninterrupted power supply (UPS) systems and emergency backup operations.

Government initiatives supporting transportation infrastructure and commercial vehicle upgrades in several countries are also contributing to market growth, particularly in emerging economies.

Top Segment: Product Type

Flooded Batteries Lead with Around 45% Market Share

Flooded lead acid batteries remain the dominant product segment due to their affordability, durability, and suitability for conventional automotive and industrial applications. Their cost efficiency and long-established manufacturing processes continue to support widespread global adoption.

Other battery types such as AGM and VRLA batteries are also gaining traction due to their maintenance-free design, improved cycle life, and enhanced performance in start-stop vehicle systems and backup power applications.

Leading Application: Transportation Sector (~40% Share)

Transportation represents the largest application segment for lead acid batteries, accounting for around 40% of total market demand in 2026. Vehicle starter batteries remain the most common application, particularly across passenger cars, commercial vehicles, motorcycles, and hybrid vehicles.

The consistent replacement cycle of automotive batteries ensures recurring demand, making transportation the cornerstone of global lead acid battery consumption.

Regional Development: Asia Pacific, North America, and Europe Drive Expansion

Asia Pacific continues to emerge as a key growth hub for the lead acid battery market, supported by strong automotive production, growing telecom infrastructure, and expanding industrial activities.

-

India: 7.2% CAGR driven by vehicle production growth, telecom expansion, and electrification programs

-

China: 6.2% CAGR fueled by large-scale battery manufacturing and automotive demand

-

United States: Stable growth supported by strong replacement battery demand and a mature recycling ecosystem

-

Japan: Growth supported by industrial applications and advanced battery recycling systems

India is expected to be one of the fastest-growing markets due to increasing automobile sales, government initiatives supporting transportation modernization, and rising demand for backup power systems across urban and rural infrastructure.

Challenges, Trends, Opportunities, and Drivers

Drivers

-

Rising demand for reliable energy storage in automotive and industrial sectors

-

Increasing deployment of telecom infrastructure and backup power systems

-

Strong global recycling ecosystem supporting sustainable battery production

Opportunities

-

Development of advanced lead acid battery technologies such as AGM and VRLA

-

Expansion of stationary energy storage applications

-

Growth in emerging markets with rising power reliability requirements

Trends

-

Increasing integration of maintenance-free battery designs

-

Adoption of improved recycling and circular economy models

-

Expansion of battery applications in hybrid vehicles and industrial systems

Challenges

-

Growing competition from lithium-ion battery technologies

-

Environmental concerns related to lead handling and disposal

-

Need for technological upgrades to maintain competitiveness

Country Growth Outlook (CAGR 2026–2036)

-

India: 7.2%

-

China: 6.2%

-

United States: Moderate growth driven by replacement demand

-

Japan: Steady growth supported by industrial applications

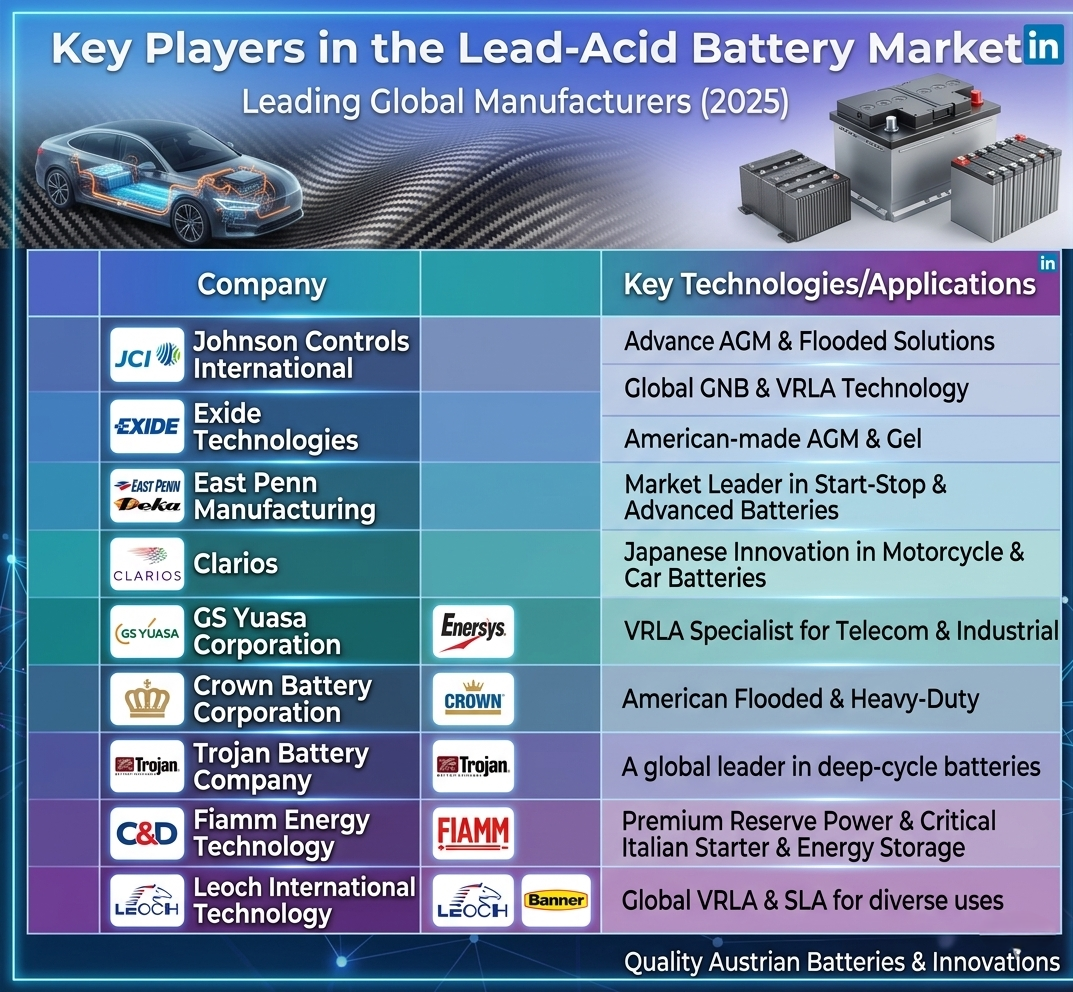

The Competitive Environment

The lead acid battery market remains competitive, with manufacturers focusing on product innovation, manufacturing efficiency, and recycling integration to strengthen their market positions.

Leading companies include Clarios, Exide Technologies, East Penn Manufacturing, GS Yuasa, and EnerSys, which maintain strong market presence through advanced production capabilities, established distribution networks, and efficient recycling operations.

Companies are increasingly investing in battery performance improvements, supply chain optimization, and environmentally responsible recycling technologies to remain competitive in a rapidly evolving energy storage landscape.

For a comprehensive strategic outlook and detailed analysis of emerging battery technologies shaping the industry through 2036, readers can explore the full report on the official Future Market Insights website:

https://www.futuremarketinsights.com/reports/global-lead-acid-battery-market